Retain Media’s Q1 2026 Marine Market Brand Consideration Report is now available, drawing on 94 brands, approximately 31,000 keywords, and more than 1.47 million searches across Australia’s marine sector.

“Q1 2026 was a quarter where the headline positions told one story and the segments beneath them told another,” said Brian Sullivan, Director at Retain Media. “Sea-Doo and Yamaha held their familiar positions at the top, but the more interesting data sat further down the table. Three wake boat brands recovering simultaneously is not a coincidence, and the propulsion segment’s quiet multi-quarter compression is a pattern that dealers and distributors will want to understand before it becomes more pronounced.”

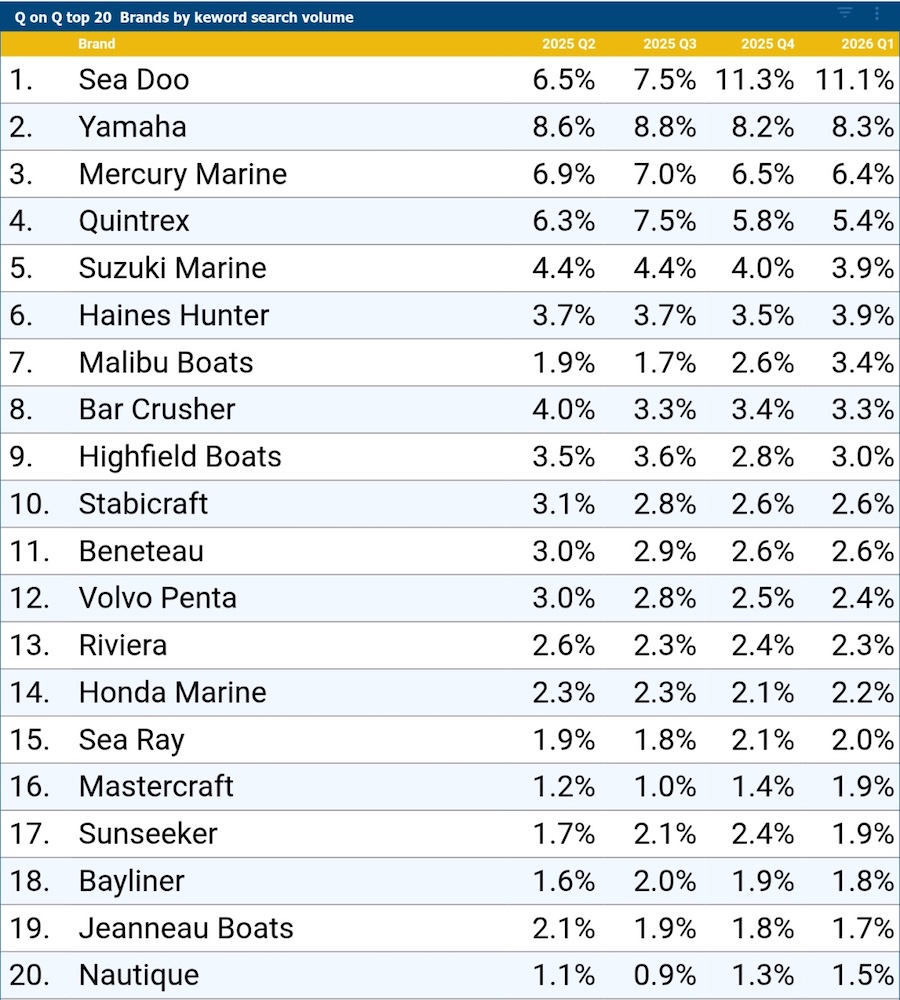

Sea-Doo and Yamaha Hold the Top of the Table

Sea-Doo held 11.1% in Q1 2026, easing just 0.2 percentage points from its Q4 2025 high. That Q4 2025 reading was the brand’s strongest across all of 2025, and retaining nearly all of it into Q1 2026 points to an audience that stays engaged well beyond the summer peak. Together, Sea-Doo and Yamaha, which steadied at 8.3% after sequential declines through the second half of 2025, accounted for roughly 19% of all marine search share in Q1 2026.

Wake Boats Deliver a Broad-Based Category Recovery

It is uncommon for three competing brands in the same niche to record meaningful gains simultaneously, but that is precisely what the wake boat segment delivered. Malibu Boats climbed from 2.6% to 3.4%, Mastercraft rose from 1.4% to 1.9%, and Nautique continued its recovery to 1.5%, all extending gains from Q4 2025 into a second consecutive quarter. When competing brands move in the same direction together, it suggests consumer appetite for the category itself is growing. The Q3 2025 dip now looks more like a temporary slowdown than a lasting shift, with ABS household spending data from that period suggesting Australians were pulling back on big-ticket purchases.

Haines Hunter Rises, but the Picture Requires Context

Haines Hunter rose from 3.5% to 3.9% in Q1 2026, a quarter that also saw the brand’s factory fire on January 9. Some of that movement may reflect information-seeking around the recovery process, though a 0.4 percentage point gain is not the kind of spike that points unambiguously to a single cause. Gradual brand awareness growth is an equally plausible explanation, and the Q2 2026 result will provide a cleaner read on the brand’s trajectory.

Propulsion Brands Compress Quietly

Mercury Marine eased to 6.4%, extending a contraction underway since Q3 2025. Suzuki Marine arrived at 3.9% after four consecutive quarters of marginal decline, and Volvo Penta fell to 2.4% from 3.0% in Q2 2025. One plausible reading is that Japanese outboard brands have been capturing a growing share of consideration traffic, though search data alone cannot confirm that with certainty. Yamaha’s minor uptick to 8.3% was the one directional exception in the category, and whether it represents genuine stabilisation will become clearer as the year progresses.

Download the full Q1 2026 Marine Market Brand Consideration Report

A Note on Methodology

This report was produced using a range of keyword research tools to assess search volume across Australia for Q1 2026. Our dataset included 94 marine brands, over 30,000 relevant keywords, and more than 1.4 million searches across the quarter.

Please note that our keyword lists and data sourcing methods are continuously evolving as we work to enhance the accuracy and depth of our search volume reporting. All data is refreshed with each quarterly report, so figures within any given edition reflect the most current available snapshot. As such, some metrics may shift quarter-over-quarter as these refinements are applied.

Bear’s State of the Industry

Australian fishing and boating legend John ‘Bear’ Willis is back to give us his take on the industry and the Q1 search results shaping 2026.

I must open with a hearty congratulations to all those who contributed to or attended the recent 2026 Sanctuary Cove International Boat Show. SCIBS truly defied a restless world of uncertainty on so many levels, with our industry tackling market opportunities head-on with a vibrant display of our wonderful Australasian boating Industry.

It has been revealed that over 41,000 visitors experienced the wonderful SCIBS event from 21–24 May. SCIBS is undoubtedly the Southern Hemisphere’s largest four-day marine event.

From my experience, I was proud to be part of an industry putting its best foot forward with a very positive display of products and services, and it seems there were many genuine buyers amongst the ‘prop spinners!’

The organisers claim that ‘the show delivered an impressive showcase, featuring:

-

-

- Sold-out exhibition

- Sold-out hospitality zones

- Over 70 new products and vessel launches

- Increase in genuine buyers through the gates.’

-

For me, a diehard fisho, it was terrific to see the return of the iconic Caribbean Boats with their new 40’ and 27’ models now produced by the strength of Maritimo, and being managed and sold by some long-standing industry greats.

The effort put into both the on-water and land-based displays was phenomenal, with impressive static and on-water displays from global brands, newcomers, and regulars alike.

Sanctuary Cove organisers also said, ‘Riviera celebrated a $40 million showcase of 12 luxury motor yachts, including the global debut of the 6200 Sport Yacht and Show premiere of the 5600 Sport Yacht.’ Meanwhile, stories abound of successes, including local favourite Sailfish Catamarans, which were quoted to have returned over $2m in sales.

Reports from the many and varied land-based exhibitors are hard to compile; however, many dealers and manufacturers were celebrating both immediate successes and looking forward to positive ongoing enquiries. From my discussions, the premium end of the market seems to be forging forward, while the more generic, ‘mum and dad’ market is tough, competitive work.

Hence, it seems that overall, the negative worldwide events experienced particularly over the first quarter of 2026 are reportedly taking some toll on many marine sales and travel; but, it’s clear that dedicated boaters are still venturing to the briny with their craft, albeit sometimes with reduced range due to fuel costs and economic inflation.

Our Q1 2026 Marine Market report indicates that many would-be purchasers are still either planning, researching, or simply fantasising over their next marine purchases and activities. This comprehensive report provides search engine results for the marine sector over the first quarter of the calendar year, as well as an evaluation of the preceding 12 months.

The good news is that enquiry and research results remain quite strong, indicating customer intent when the world returns to a more normal structure. While fuel prices and availability, plus inflation, have certainly taken a toll on effort, it seems many dedicated marine users have embraced the ‘new norm’ and are returning to their adventurous lifestyles. Myself included.

Tight lines!

Bear.

The 20 Most-Searched Marine Brands in Australia

Where the Market Stood in Q1 2026

Four quarters of search data tell a story of a market in motion. Sea-Doo and Yamaha continue to command the top of the table with a combined share that leaves the remaining 18 brands competing for the majority of consideration traffic, while the middle of the rankings shows considerably more movement than the headline positions suggest.

Brand Performance by Segment

Personal Watercraft

Sea-Doo held the top position in Q1 2026 with 11.1%, easing just 0.2 percentage points from its Q4 2025 high of 11.3%. That Q4 2025 reading was the brand’s strongest across all of 2025, built on peak summer demand as Australians planned their time on the water. Retaining nearly all of that share into Q1 2026 is notable. A more pronounced seasonal correction would not have been surprising, and its absence points to an audience that stays engaged with the brand well beyond the summer peak. Combined with Yamaha, Sea-Doo accounted for roughly 19% of all marine search share in Q1 2026. For the 18 brands below them, that concentration defines the competitive landscape they are working within.

Together, Sea-Doo and Yamaha accounted for roughly 19% of all marine search share in Q1 2026, a concentration at the top of the market that leaves the remaining 18 top-20 brands competing for roughly 80% of total consideration traffic.

Propulsion Brands

Yamaha held second position in Q1 2026 with 8.3%, a marginal 1.2% relative uptick from Q4 2025 readings. The movement is small, but it is directionally notable for a brand that had been recording sequential quarterly declines through the second half of 2025. Whether that uptick reflects genuine stabilisation or simply quarterly fluctuation will become clearer in Q2 2026, but for Yamaha’s dealer network, consistent top-two placement across consecutive quarters provides a stable foundation for prospect-nurturing activity regardless of the minor oscillations around it.

Mercury Marine observed a quarterly movement from 6.5% to 6.4%, extending a contraction that has been underway since Q3 2025. The gap between Mercury Marine and Yamaha has widened slightly, sitting at 1.9 percentage points this quarter compared to 1.7 percentage points last quarter. Mercury Marine’s gradual quarterly easing across three consecutive quarters suggests buyer preference in the outboard motor category may be consolidating further around Yamaha, a consideration worth observing as we move into Q2.

Suzuki Marine eased to 3.9% in Q1 2026 from 4.0% in Q4 2025, now sitting 0.5 percentage points below its Q2 2025 reading of 4.4%. Four consecutive quarters of marginal decline is a pattern worth monitoring, even when each individual movement appears small. The propulsion category’s buyer behaviour is inherently stable, and that stability cuts both ways. Entrenched brand preferences are difficult to erode, but they can also be difficult to rebuild once consideration share has been ceded over an extended period. For a brand in Suzuki Marine’s position, the data points to a closer look at what is driving the gap with the two propulsion brands above it.

At 2.4% in Q1 2026, Volvo Penta has now declined 0.6 percentage points across four consecutive quarters. That trajectory runs in parallel with the gradual easing recorded by Suzuki Marine, and one plausible reading of both trends is that Japanese outboard brands have been capturing a growing share of mid-funnel consideration traffic across the research journey. Whether that dynamic is the primary driver or other factors are at play is difficult to determine from search data alone, but the parallel movement across two distinct propulsion brands is a pattern to keep an eye on.

Additionally, Honda Marine bucked the propulsion trend with a minor uptick to 2.2% from 2.1% in Q4 2025, a small but welcome move after several softened quarters and probably hastened by new product promotions.

Trailer Boats

Quintrex arrived at 5.4% in Q1 2026 after a second consecutive quarter of correction from its Q3 2025 peak of 7.5%. The brand’s lead in the trailer boat category remains commanding, as it still holds nearly double the search share of its nearest rival. Whether the softening points to a post-peak normalisation or a structural shift will become clearer in Q2 2026.

The more ambiguous result belongs to Haines Hunter, which rose to 3.9% from 3.5% in a quarter that also saw the brand’s factory fire on January 9. Some of that movement may reflect information-seeking around the recovery process, though a 0.4 percentage point gain is not the kind of spike that points unambiguously to a single cause, and gradual brand awareness growth is an equally plausible explanation. Both readings are worth holding simultaneously as we head into Q2.

Further down the table, Bar Crusher eased to 3.3%, Highfield Boats recovered to 3.0% from 2.8%, and Stabicraft held flat at 2.6% for a second consecutive quarter. All three brands are broadly stable, with Highfield’s modest recovery the only notable movement after its sharp pullback last quarter.

Performance and Wake Boats

It is uncommon for three competing brands in the same niche to record meaningful gains simultaneously, but that is precisely what the wake boat segment delivered in Q1 2026. Malibu Boats climbed to 3.4% from 2.6%, Mastercraft rose to 1.9% from 1.4%, and Nautique continued its recovery to 1.5%, all extending gains from Q4 2025 into a second consecutive quarter.

When competing brands move in the same direction together, it suggests consumer appetite for the category itself is growing rather than buyers simply shifting preference between brands. The Q3 2025 dip now looks more like a temporary slowdown than a lasting shift, with ABS household spending data from that period suggesting Australians were pulling back on big-ticket purchases. Whether that connection holds as a repeatable pattern is something the data will either confirm or challenge as the year progresses. For dealers and distributors in this category, the window for conversion-focused activity is open now.

Luxury Yachts and Sailing Brands

Sunseeker retreated to 1.9% in Q1 2026 from 2.4% in Q4 2025, a 20.8% relative decline and the sharpest single-quarter pullback in the top 20 outside the propulsion category. The scale of the drop is notable given the brand had been building search share steadily across 2025. Some seasonal softening in luxury yacht consideration is expected as the boating season winds down, but Sunseeker’s correction is considerably larger than Riviera’s, which eased only slightly to 2.3% from 2.4% across the same period. One possible explanation is that Sunseeker’s Australian search interest is more heavily concentrated in the peak boating season, though whether that reflects differences in audience, content strategy, or market positioning is difficult to determine from search data alone.

Beneteau held steady at 2.6% for a second consecutive quarter, while Sea Ray pulled back modestly to 2.0% from 2.1% in Q4 2025, a minor correction following its strong Q4 2025 recovery.

Notable Movers and Brands to Watch

Outside the movements covered above, Mastercraft’s recovery arc deserves to be highlighted in the context of the full table. Outside the movements covered above, Mastercraft’s recovery arc deserves to be highlighted in the context of the full table. The brand entered the tracking period in Q2 2025 at 1.2%, dropped to a year-low of 1.0% in Q3 2025, and has since recovered to 1.9% across two consecutive quarters of gains, closely mirroring Malibu Boats’ trajectory. Nautique’s continued climb to 1.5% makes it three from three in the segment.

Worth noting further down the table is Jeanneau Boats, which slipped to 1.7% in Q1 2026 from 1.8% in Q4 2025, extending a gradual decline from its Q2 2025 reading of 2.1%. Having shed 0.4 percentage points across four consecutive quarters, the brand’s trajectory runs parallel to Volvo Penta’s. Whether both trends reflect a broader softening in European brand consideration among Australian buyers, or whether other factors are at play, is difficult to determine with these findings alone. However, the consistency across two distinct European brands deserves monitoring in future quarters.

Movement at the Margins

The top-line figures in Q1 2026 only tell part of the story. Beneath them, different segments are responding to different conditions and moving at different speeds. Propulsion brands are stable but quietly compressing. The luxury segment is seasonal, and not all brands appear equally equipped for the off-peak months. The trailer boat category is correcting from a promotional peak while absorbing an external event that clouds its near-term direction. The wake boat segment, meanwhile, looks less like a group of brands rebounding individually and more like a category regaining broader momentum.

Across all of it, the brands best placed to capitalise are those with a clear picture of what is driving their search audience and whether that visibility is converting into active consideration. For those still building that picture, the data is a useful place to start.

For more information on Retain Media, visit retainmedia.com.au